This week, I had the great honor of being a main platform speaker for a national conference of top investment and insurance professionals. One of several ideas I shared was a strategy that – judging from the reaction of listeners – no one in the audience had ever heard of before!

This week, I had the great honor of being a main platform speaker for a national conference of top investment and insurance professionals. One of several ideas I shared was a strategy that – judging from the reaction of listeners – no one in the audience had ever heard of before!

I refer to it as the “Forty-Year Tax-Deferred Installment Sale.” It’s a powerful tool for allowing the sale of an appreciated asset such as real estate, a business, or other specific, appreciated assets (such as your antique car collection … the one in the garage, NOT the backyard) while deferring the recognition of taxes for as long as 40 years.

To illustrate the power of this idea, let’s have a look at a developing case study for Jack and Jill Hill. They are a lovely couple in central California who are selling their business and the accompanying office building.

Selling appreciated assets now and deferring the taxes while growing the assets for 40 years … Imagine That!™

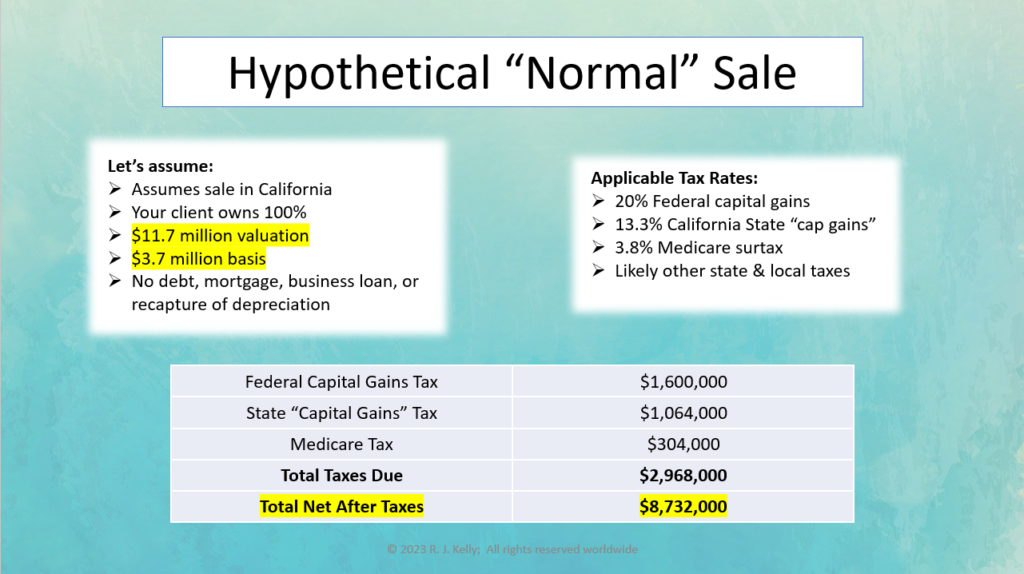

Framing the Sale Solution

Here is the background on the case:

- Selling business & office building in Oakland (they miss the Raiders & the A’s)

- Facing 37.1% taxes on appreciated value of both the business and the office building

- 1031 Exchange not an option for a business sale & a difficult environment for the sale of this real estate

- Business valued at $6.7 million

- Office building valued at about $5 million

If we assume $3.7 million in basis, no debt, mortgage, business, loan, or recapture of depreciation, then we’re looking at $8,732,000 net after the $2,968,000 in taxes. (Trust us, the math checks out.)

This is a very specialized strategy. It has some unique rules beyond what we love in using life insurance as a tax-free income stream. So, let’s dive into the nitty gritty details and see if this might be a smart strategy for your wealth-building, estate planning, or even business succession planning.

How, exactly, do we defer that nearly $3 million in taxes for 40 years?

Income Now, Taxes Later

We took a deep dive into how this strategy worked last month. Here’s the link again, in case you want to take a detour.

But here’s the gist:

Step 1: Structure the sale as an installment sale with an assignment provision

Step 2: Seller transfers the asset and title into escrow

Step 3: Buyer sends the cash to escrow

Step 4: Asset and title to go the buyer, and they go on their merry way

Step 5: Escrow transfers the installment sale to the assignment company along with the net cash from the buyer (after escrow takes out their couple bucks for closing costs, etc.)

Step 5 is clearly a doozy. It’s where all of the magic happens.

But rather than repeat ourselves, we want to dive into how the money gets back into the buyer’s hands.

Part of Step 5 uses something called … brace yourselves since it might be a new concept for many readers … a “Private Placement Variable Life Insurance” (PPVLI) contract or a “Private Placement Variable Annuity” (PPVA).

Let’s start with the life insurance option.

What is a Private Placement Variable Life Insurance Contract?

The current life insurance contracts that are out there today are certainly much more high-performance than our parents’ contracts could ever consider being. However, this type of Private Placement Life Insurance contract leaves even today’s hybrid life insurance contracts at the starting line, wondering what happened.

Let’s pretend regular life insurance is a cute little bi-plane – complete with the pilot’s goggles hanging off the propeller. It goes faster than a car or train and makes transportation great if a little cold in the winter.

Now, picture getting launched off an aircraft carrier (I have gotten to do that, and it is a total rush!) With all of the advanced abilities of the PPVLI and especially with the ability to invest in almost anything, instead of buckling into your trusty bi-plane, you’re firing off in a jet. You can still wear the goggles if you want. But the point is you’re going much, much faster.

If you understand this instrument, skip the next paragraph. If it’s new to you, get the basic structure below.

When you correctly design a life insurance contract to minimize the death benefit but maximize the premiums, you normally build cash values much faster. When enough time has elapsed after supercharging that contract, you can borrow against the cash value and never have to pay it back. (It just gets subtracted from your survivor benefit.) But, because it’s a loan (0% – 0.25% interest), the IRS does not consider it income.

I’m sure you can imagine the possibilities, but many of our clients enjoy using their life insurance as a tax-free income stream to supplement their retirement income. No Medicare penalties. No social security considerations. Just cash!

One of the most attractive features of a PPVLI is that you can invest in almost anything. A more traditional style of life insurance contract limits you to indexes or equities. But here you can invest in:

- Hedge funds

- Private equity funds

- Bonds

- Fixed-income securities

- Real Estate

- Commodities

- And yes, regular old equities

But here’s the catch … of course, there’s always a catch, right? Okay, you got me. There are actually two here …

First Catch: Diversification Rules

So, maybe this one isn’t a big deal. But it’s a pitfall to be aware of.

You cannot be invested into only one asset. You have to be invested in a range of assets, as shown below. Not “all your eggs in turkey futures,” for example, even if Thanksgiving is fast approaching.

You have one year from the date you sign the contract to meet the diversification test. Some classes of real estate investing have longer time frames because real estate can take … well … time.

Here are the specifics:

- A single asset must be less than 55% of the overall value of the annuity assets

- Two assets must be les than 70%

- Four assets must be less than 90%

When we are in the investment seat as portfolio advisor, this is easily avoidable. We will normally be fully diversified in a variety of asset classes, neatly avoiding the IRS’ displeasure.

Speaking of which, what are the penalties?

If you fail the diversification test, the contract is no longer considered life insurance, and you get a “retroactive assessment of taxation” at ordinary rates, plus fees and interest. Yikes!

Second Catch: Investor Control Doctrine

The good news is this second catch cleverly prevents you (in most cases unless you’re hiring a random person off the street as your investment manager) from failing the diversification test.

And that is … you simply cannot direct your own investments.

In 2015, the U.S. Tax Court heard the case Webber v. Commissioner. This case, plus 30 years of IRS “Private Letter Rulings,” determined that the owner of a PPVLI cannot direct investments within that contract. Neither can they “have an arrangement, contract, plan or agreement” with their investment advisor (and/or accountant and attorney) to select or direct investments within the PPVLI.

However, a client can provide their “philosophical preferences” in the abstract and their risk tolerance in the specific to help the advisor better know the types of investments that would be appropriate for this advanced planning strategy.

You can give your investment advisor a good indication of what is and is not acceptable to your investment goals and philosophy. Ultimately, working with someone you trust and have a good relationship with will help this go smoothly. And if not, you can always fire them and hire someone else!

Personally, as a Registered Investment Advisor, I (and our whole team) go to great lengths to understand risk tolerance and other important considerations long before we would raise the prospect of utilizing such a powerful strategy.

Now, for a few people, this might sound scary. Especially if you’re used to being in complete control over all of your investments. As a fiduciary, most of our work is getting to know our clients and making sure they’re diversified. We want to help take the hours involved off their plate so they can use that time to do what they find meaningful.

In short, if you need complete control over your investments, this might not be the strategy for you. If you have worked with financial advisors in the past and they have been attentive to your needs, goals, and personal philosophies, then this rule is no different than how you’ve already been growing your wealth.

So … should you be “the guy” who sends over 70,000 emails trying to direct how to invest the money inside this insurance “wrapper” (I am not kidding. One guy sent over 70,000 emails … Sheesh. I would lose his phone number!) that is a violation. That is called the “Prohibition of Investor Control Doctrine.” The penalties are the same as violating the diversification rule—retroactive tax assessment at ordinary rates, fees, and interest.

PPVLI Tax Treatment

PPVLI contracts, unless the laws change, are treated just like regular life insurance contracts.

Your distribution is not recognized as taxable income so long as:

- You’re not paying in too much in the early contract years to accidentally create a “Modified Endowment Contract” (MEC)

- The contract is properly structured to meet the IRS’ definition of life insurance

- A single asset must be less than 55% of the overall value of the annuity assets

As a bonus, the survivor benefits going to your beneficiary is not included in the recipient’s gross income or taxed as capital gains income … and with a little more creativity, we can usually make the survivor benefit not includible for estate taxation!

All good things! But wait, what about the annuity option?

What Is A Private Placement Variable Annuity?

A Private Placement Variable Annuity (PPVA) is similar to the PPVLI, except it falls under the tax laws for an annuity instead of life insurance. (No snickers. I know this sounds like a “duh,” but did want to make that point.)

To start, that means that you aren’t paying for the death benefit, and there’s no medical underwriting. Nice!

But here’s where it gets fun.

PPVA also differs from regular annuities. In most regular annuities, you’ll find extra features like income guarantees or principal protection. In the spirit of no free lunches, these features add costs. Using a private placement annuity means you get the tax advantages AND much lower fees overall.

The PPVA has all of the same perks as the PPVLI. Namely, you can invest in alternative investments that are “tax-inefficient” outside of a retirement account, e.g., short-term capital gains on stocks, dividends, interest, etc., However, because of the “tax wall” of the annuity, there is no tax until/unless withdrawals are taken from the annuity!

When you begin to take income, it is taxed as “last in – first out.” LIFO treatment. Translated, this means whatever is earned as realized income is taxable as ordinary income … even if it is long-term capital gain! Only when all the earnings are tapped and paid out do you get into the principal and non-taxability.

And, one last thing to keep on the radar screen … if you are younger than 59½ and want income, there is a 10% penalty tax in addition to having the income taxed as ordinary income. As always, with complex tax situations, speak with your tax professional!

For both PPVLI and PPVA, you’ll need a “Separately Managed Account” or SMA run by a Registered Investment Advisor (RIA). Remember the prohibition on the Investor Control Doctrine? That applies here, too.

Both PPVLI and PPVA have another significant advantage. They have a SMA by a professional that isn’t affiliated with the insurance company. The assets are protected against creditors to the extent of your specific state’s law, both from your creditors and the life insurance company’s creditors.

Some states provide 100% asset protection. Other states limit the amount of creditor protection afforded for life insurance and annuities. Do check your own state’s limitation or the state in which you situs the trust holding the asset, like Delaware, South Dakota, or Nevada.

But here’s where it gets even better for the philanthropists among us.

If you name a charity as the beneficiary of the PPVA, all of the investment gains go to the charity tax-free at the time of the owner’s death. PLUS, unlike other philanthropic tools, the PPVA remains under the owner’s control (and surviving spouse) for their lifetimes. Yay!

So you get both the tax-advantaged income AND the rest goes to making the world a little better.

How Would This Look For The Hill Family?

Now that we’ve been through the details let’s go back to our friends in Oakland. Would they do better to pay the tax now or defer it for 40 years?

Here’s a refresher on the sale numbers and what they would pay under the current California and Federal tax codes.

Woah. Makes your head spin a little, right?

But the real $64,000 question, or rather the $11 million dollar question, is …

… how does the math work out?

What would their income be like if they just paid the tax upfront versus the deferral of 40 years?

Assuming a 5% withdrawal from their annuity and a 7% growth rate. Here’s what their income would look like over the next 40 years from selling their business.

Oh, and just for fun, we went ahead and calculated the taxes (at current rates, who knows about the coming decades) for both Federal and California income tax.

So … if your brain is going to mush right now, here’s the bottom line. It makes more sense to wait to pay taxes until the end of 40 years than it does to pay them now!

Sorry … didn’t mean to shout. Just wanted to make a point. Eh???

But what if taxes go up, you ask? (Clever you! Great question!!)

Only if combined taxes rise above 72% would it be better to pay the taxes now than wait. So, if you see tax rates starting to dramatically increase, or hints of it, you may want to pull the trigger and not wait the full 40 years before reporting the gain on the sale of your real estate/business/appreciated asset.

Hey … one more thing. This doesn’t work for the sale of publicly traded stocks or bonds. Bummer. Notice I said publicly traded stocks or bonds. Privately held stocks, however, would be an excellent choice for using this concept.

Almost There! What Situations Make The Private Placement Strategy Shine?

First, if one or more of the following apply to you, we should have a chat.

You want …

- A long-term tax diversification strategy

- Improved tax efficiency on your investments

- Tax-efficient investing following a liquidity event

- Future, supplemental income

- A plan for wealth transfer with liquidity

- Alternative asset investments

- Life insurance for estate planning, tax mitigation and/or other income that is tax-favored

- To multiply your gifts to charity upon your death – which could be your own generational family giving fund

So … can anyone do this???

Sorry … no. One more catch. To qualify to purchase either a private placement life insurance or annuity contract, you must be an “accredited investor.” The IRS believes that because you have so many investment options (i.e., potentially higher risk, higher reward), only folks who are in a better position to absorb any potential losses get to wear the party hat.

Accredited investor means that one of the below applies:

- You have $1 million of assets NOT counting the equity in your home

- Or, you have generated $200,000 of income per year if single for the last two years plus the current year

- Or, $300,000 combined incomes per year if married for prior two years and current year

- Or, a financial advisor with either a Series 7, 65, or 82 license

Here are the most common situations in which a PPVLI/PPVA makes good investment sense.

Estate Planning – using an Irrevocable Life Insurance Trust (ILIT) to move wealth out of your estate and transfer it to future generations while minimizing estate taxes is a well-loved strategy. Using a PPVLI in combination with it lets you transfer even more.

Asset Protection – Depending on the state (ask us about domicile!) the assets with your contract may be 100% protected from creditors!

Philanthropy – You can fund a PPVLI/PPVA with the intention of a charity being the final recipient of the funds. You can either name a charity as the final recipient or transfer ownership of the contract.

Business Succession Planning – PPVLIs can fund buy-sell agreements.

Tax-Deferred Growth – what’s not to love? No taxes on the growth within the contract.

Tax Diversification Strategy – Some investments (hedge funds and private equity, to name a couple) are extremely tax-inefficient. If your investment manager selects these for your contract, you’ll likely get better returns because of the tax treatment.

On a side note. There is nothing stopping someone from setting up both a PPVLI and a PPVA. If you’re like me and can’t decide between the chocolate cake and the strawberry cream cake, you can (in this case) get both, calorie-free!

What About Your Appreciated Assets?

Well, that was a lot! Here’s a chart in case we lost you for a few hundred words.

While there are a lot of moving parts, it’s a fairly straightforward process with the right team in place. And, if you happen to be in the agricultural space, you get an even better version of this strategy thanks to some changes Congress made in the late 80s.

Oh, and on choosing between the life insurance and the annuity? Jack and Jill Hill are going with a 60/40 mix … write us and tell us which way you think the split went!

If you have any questions about options for selling your appreciated business or other assets, reach out to schedule a complementary 20-minute consultation! This idea is one of a number of options. There is no one perfect solution for everyone, and it is oftentimes a combination of ideas.

Deferring the taxes will most often net you waaaaaaaaay more money both today and down the line. You can keep the IRS off your back and their hands out of your wallet for decades … Imagine That!™

Imagine That!™ is a complimentary monthly newsletter provided by Wealth Legacy Group®, Inc. that addresses various topics of interest for high-net-worth and high-income business owners, professionals, executives and their families. Sign up to receive our monthly newsletter here.

R. J. Kelly, Wealth Legacy Group®, Inc. – October 2023

Header image on Canva, one design use license