It seems I am hearing more and more often the question, “How much can I take out of my retirement account(s) and assets without running out of money?”

It seems I am hearing more and more often the question, “How much can I take out of my retirement account(s) and assets without running out of money?”

Fortunately, we have a book coming out in the next few months that addresses that and a whole bunch more! It’s called, Creating Your Ideal Retirement – Starting Today! Overcoming the Biggest Planning “Frictions” That Will Keep You From Retiring Well.

To answer the question, here’s an excerpt from the upcoming book….

We have a new client that we’ll call Tom. He came to us frustrated by the low returns he has received over the last 20 years working with a certain advisory group. Quite literally, his annualized return after all those years was just over a quarter of 1% per year. Ouch!

He wanted to know, could we do better for him?

I said …

“Tom, it sure wouldn’t take much to do better than what’s happened here.” So, I showed him using back-tested returns, and actual historical data, how his assets would have grown had he been working with us over that same 20 years. Net of all fees, including mine, it would have been over 9.5% per year.

Are you like Tom? Have your returns been disappointing over the years? Even if your returns have been favorable, are you concerned that you may run out of money down the road? Do you have the research data to back up what percentage withdrawal is “safe” over time? How about what percent can you increase your annual withdrawal without negatively affecting the safety of your principal?

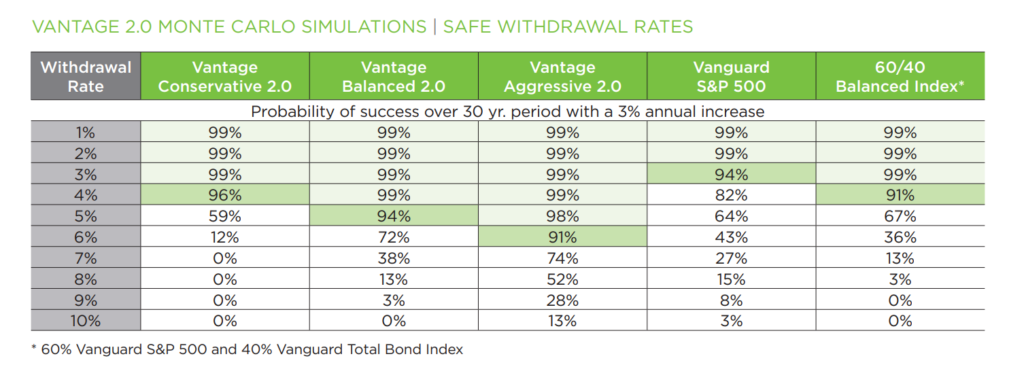

By utilizing a platform (like the one we use here at Wealth Legacy Group®, Inc.,) we can actually increase your withdrawals by as much as 50% more than “conventional wisdom” – while still having a “confidence factor” (the confidence of not running out of money!) of over 90%.

As an illustration, the chart below compares the historical returns of three different allocations from our preferred investment platform – Vantage Conservative – Vantage Balanced – Vantage Aggressive. Next, we compare that to the vaunted Vanguard S&P 500 Index fund and the traditional 60/40 mix of stocks/equities versus bonds/fixed income. We then “stress test” each of the portfolios over a 30-year period and include a 3% annual Cost-of-Living-Adjustment (COLA.) After all that, we determine the statistical probability that there is still money left in our investment portfolio after 30 years.

Why? Because running out of money is NOT an “ideal retirement!”

The statistical analysis below has a fancy name. It is called a “Monte Carlo simulation,” and with the aid of lightning-fast computers, runs thousands upon thousands of iterations to determine the likelihood of certain financial outcomes.